When Trillions of Passive Dollars Follow Index Rules, Who Decides the Rules?

By CoinEpigraph Editorial Desk

As anticipation builds around a potential SpaceX public offering, a broader debate is emerging across financial markets. The discussion is no longer centered solely on valuation. It is increasingly focused on how index providers, passive investment vehicles, and benchmark methodologies may influence the flow of trillions of dollars into the next generation of mega-cap companies.

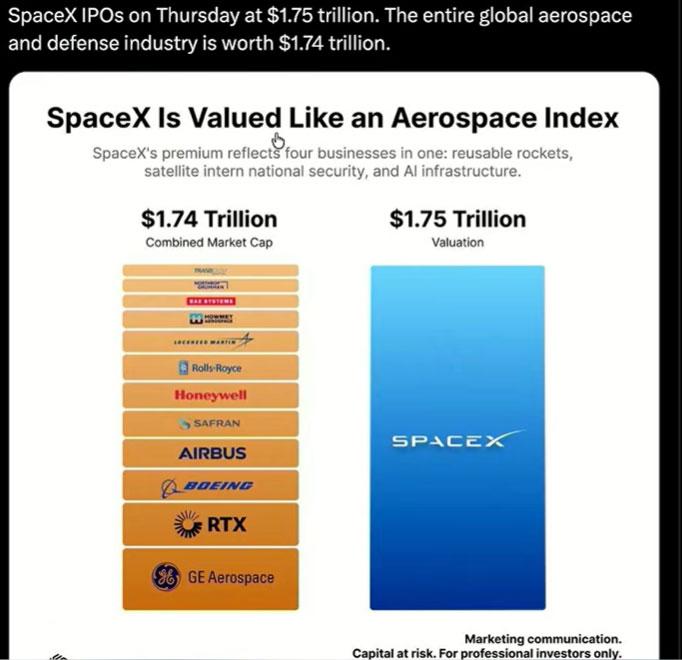

The scale of the proposed valuation has itself become a subject of discussion across institutional circles. A comparison circulating among investors suggests SpaceX would enter public markets at a valuation roughly comparable to the combined market capitalization of many of the world’s largest publicly traded aerospace and defense companies, including Boeing, Airbus, RTX, Lockheed Martin, Northrop Grumman, General Dynamics, Honeywell, Safran, and others.

The observation is less a statement about aerospace than it is a reflection of how difficult SpaceX has become to categorize. Investors are no longer valuing the company solely as a launch provider or aerospace manufacturer. The valuation increasingly reflects exposure to launch services, satellite communications, national security infrastructure, and broader assumptions surrounding future global data networks.

The discussion may appear technical.

Its implications are not.

In recent months, several major index providers have either adopted or confirmed mechanisms that could allow exceptionally large newly public companies to enter benchmark indexes more rapidly than was historically common. Nasdaq has introduced accelerated inclusion pathways for certain mega-cap offerings. FTSE Russell has modified portions of its framework to facilitate faster consideration of large IPOs. MSCI has confirmed that companies of sufficient scale may qualify for expedited inclusion under existing methodologies.

At the same time, S&P Dow Jones Indices declined to relax its own seasoning and profitability requirements, preserving a more traditional approach to index eligibility.

Viewed individually, these decisions may appear procedural.

Viewed collectively, they have sparked a broader conversation about who ultimately determines the flow of passive capital through modern markets.

The Rise of Passive Power

The significance of this debate becomes easier to understand when viewed through the lens of passive investing.

For much of the twentieth century, active portfolio managers served as the primary mechanism through which capital entered public markets. Analysts evaluated companies, fund managers made allocation decisions, and investors consciously chose where to deploy capital.

That landscape has changed dramatically.

Today, trillions of dollars reside within index funds, exchange-traded funds, pension allocations, retirement accounts, sovereign wealth portfolios, and benchmark-driven investment products. In many cases, capital moves not because a portfolio manager makes a discretionary decision, but because an index methodology requires it.

The distinction is important.

When a company enters a major benchmark, ownership can begin expanding automatically across thousands of investment vehicles simultaneously. Retirement accounts may gain exposure. Pension funds may gain exposure. Institutional portfolios tracking benchmarks may gain exposure. The movement of capital is often mechanical rather than discretionary.

That reality has transformed index construction from a largely administrative exercise into a powerful component of modern market structure.

The rules themselves increasingly matter.

Why Seasoning Periods Existed

Historically, seasoning periods served a practical purpose.

Newly public companies were granted time for markets to establish a fair valuation through open trading. Analysts initiated coverage. Investors reviewed public disclosures. Earnings reports entered the public record. Lockup periods began revealing how insiders viewed long-term ownership.

In short, markets were given an opportunity to digest information before benchmark-driven capital began arriving in size.

Supporters of accelerated inclusion argue that those frameworks were developed during an era when most IPOs entered public markets at significantly smaller valuations. A company valued at hundreds of billions—or even trillions—of dollars presents a different challenge. Excluding such firms from major benchmarks for extended periods may create distortions between indexes and the broader market they are intended to represent.

From that perspective, modernization is not only reasonable but necessary.

Critics, however, view the issue differently.

They argue that the purpose of a seasoning period has not changed simply because companies have become larger. The process of price discovery remains important. Public reporting remains important. Market stabilization remains important.

The concern is not necessarily whether SpaceX represents a high-quality company.

The concern is whether passive capital should be directed toward any newly public company before markets have had sufficient time to establish a durable valuation framework.

A Debate Larger Than SpaceX

What makes the current discussion particularly noteworthy is that it extends well beyond a single company.

The same questions could eventually apply to Anthropic.

They could apply to OpenAI.

They could apply to Databricks.

They could apply to future artificial intelligence firms, advanced manufacturing companies, defense technology platforms, or infrastructure businesses that remain private long enough to reach unprecedented scale before entering public markets.

The issue is not SpaceX.

The issue is what happens when private companies become so large that existing market infrastructure begins adapting around them.

For decades, market participants largely accepted the idea that companies must conform to the rules of public markets.

Today, some observers believe the opposite dynamic may be emerging. As private firms remain private longer, accumulate larger valuations, and command greater influence, market infrastructure itself may increasingly evolve to accommodate them.

Whether that represents healthy modernization or an emerging governance concern remains a matter of debate.

Market Structure Outlook

The SpaceX IPO may ultimately be remembered for many reasons. It could become one of the largest public offerings in financial history. It could reshape expectations surrounding private-company valuations. It could influence the future trajectory of aerospace, communications, and defense technology investing.

Yet the most consequential question may have little to do with SpaceX itself.

In a financial system increasingly dominated by passive investing, index rules have become pathways through which trillions of dollars move. Decisions that once appeared technical now influence capital allocation across retirement accounts, pension systems, institutional portfolios, and benchmark-tracking funds around the world.

That reality raises a question that is likely to outlive any single IPO.

When trillions of dollars follow index rules, who ultimately decides the rules?

The answer may help shape not only the future of SpaceX, but the future of every trillion-dollar company that follows.

At CoinEpigraph, we are committed to delivering digital-asset journalism with clarity, accuracy, and uncompromising integrity. Our editorial team works daily to provide readers with reliable, insight-driven coverage across an ever-shifting crypto and macro-financial landscape. As we continue to broaden our reporting and introduce new sections and in-depth op-eds, our mission remains unchanged: to be your trusted, authoritative source for the world of crypto and emerging finance.

— Ian Mayzberg, Editor-in-Chief

The team at CoinEpigraph.com is committed to independent analysis and a clear view of the evolving digital asset order.

To help sustain our work and editorial independence, we would appreciate your support of any amount of the tokens listed below. Support independent journalism:

BTC: 3NM7AAdxxaJ7jUhZ2nyfgcheWkrquvCzRm

SOL: HxeMhsyDvdv9dqEoBPpFtR46iVfbjrAicBDDjtEvJp7n

ETH: 0x3ab8bdce82439a73ca808a160ef94623275b5c0a

XRP: rLHzPsX6oXkzU2qL12kHCH8G8cnZv1rBJh TAG – 1068637374

SUI – 0xb21b61330caaa90dedc68b866c48abbf5c61b84644c45beea6a424b54f162d0c

and through our Support Page.

🔍 Disclaimer: CoinEpigraph is for entertainment and information, not investment advice. Markets are volatile — always conduct your own research.

COINEPIGRAPH™ does not offer investment advice. Always conduct thorough research before making any market decisions regarding cryptocurrency or other asset classes. Past performance is not a reliable indicator of future outcomes. All rights reserved | 版权所有 ™ © 2024-2029.